The latest answers to your questions

Coronavirus Relief Loan – The CARES Act’s Paycheck Protection Program (PPP)

We’re here to help keep you informed. Answers will be updated as new details become available based on guidance from the US Treasury Dept., the Small Business Administration, and lenders processing and issuing PPP loans.

- All Categories

- Application

- BoeFly

- Borrowers

- Fees

- Funding

- Lenders

- Loan

- Payroll

- Portal

- Taxes

- Technical

- Working Capital

- Loan Processing

- Banks

- Franchise

- Self-Employment

- Fund Depletion

To withdraw your application from the BoeFly portal, please log in to your account and click the withdraw icon (-) for your application, under the action column. If there is no withdraw icon in your account, please email your request to support@boefly.com.

Additionally, if you have received SBA authorization (i.e., an E-Tran number) elsewhere, we ask that you notify us at support@boefly.com. We caution you from withdrawing your application with your BoeFly lender unless you have full certainty that you have been SBA authorized as opposed to being simply approved by a bank.

Unfortunately, once an application status is changed to Lender Submitted, applications cannot be edited. The same is true for Lender Approved (Pending SBA Authorization) and SBA Approved statuses.

Each lender will have a different system for processing PPP loans, which may or may not be automated and therefore may or may not allow for direct communication to ask questions or discuss individual loans. Information about this should be available from the lender upon their direct engagement.

BoeFly, in partnership with select lending partners, has designed an online application. You will need to provide documentation in support of the average monthly payroll costs that drives your loan amount. Currently, you should be prepared to share some or all of the documentation below (depending on your business). Your secure BoeFly portal application will let you know if there is any further documentation needed.

Note: Not ALL documents are needed for every applicant (instructions are in the Portal). Date of Birth (DOB) for each owner entry is required, and a Driver’s License (image of front and back) or other government-issued identification is required for each 25% or more owner.

Employers with payroll only (no independent contractors or sole proprietors):

One item only is needed from the list below:

- The preferred option is the CARES file from your payroll provider. ADP and Paychex both have pre-prepared reports that present eligible data, or

- An IRS Form 940 for full year 2019, or

- All 4 IRS quarterly Form 941s (Only needed if Form 490 is not available)

If you were not in business by Jan. 1, 2019, provide your payroll runs from Jan. and Feb. 2020. You must have had employees on Feb. 15, 2020, to be eligible.

ONLY INCLUDE owner’s draw if it’s on your payroll report, or income noted on Schedule K-1 or Schedule C, depending upon how the entity is structured, up to $100,000 annualized is eligible to be counted in the calculation. Owner draws, distributions, and loans to shareholders who are not subject to payroll or self-employment tax are not eligible.

DO NOT INCLUDE 1099 contractors in your employee compensation – this field in the portal is only to be used by those who are self-employed (independent contractors and sole proprietors) who file for themselves. Employers cannot include independent contractors as employee compensation.

Employers or 1099 contractors/sole proprietors with other benefits:

- If you want other benefits included, provide information for healthcare (e.g., monthly statements), retirement benefits (monthly statements from the provider).

Independent contractor:

- All 1099s received for 2019

Independent contractor:

- If 2019 taxes were filed (Schedule C)

- If 2019 is not filed, P&L for 2019

All of your supporting documents should be PDFs.

For additional SBA and Treasury guidance, the Treasury Department has created a link to their own FAQ document to address specific borrower and lender questions concerning the implementation of the PPP, and it will be updated on a regular basis.

Once an application status is changed to Lender Submitted, Lender Approved (Pending SBA Authorization) or SBA Approved it cannot be edited, as the loan application has been received by a bank for processing.

To make changes to an application that has the status of Submitted, In-Progress or Created, log into the secure portal application. You will have to unlock your application to edit information or upload new documentation.

How to unlock submitted PPP applications:

- Watch this short how-to video

- Log in

- Go to your home page, review your submitted application with the view icon

- If it needs to be corrected or updated with documentation, then:

- Click the lock icon for your app

- Confirm you wish to unlock, then click the edit (pencil) icon

- Review each section carefully, including documents, then resubmit and e-sign

To update owner information, like Driver’s License or Date of Birth (DOB), follow the same process above, then navigate to the owner’s section, select edit, update the percent ownership, and ensure the DOB is correct. If the ownership is more than 25%, you will be prompted to upload a Driver’s License. You can always upload copies of the Driver’s License on the documents page as well.

The NAICS code is required on the PPP application. Watch this video for simple instructions to find and add the NAICS code.

Watch this video for simple instructions on how to edit your in-progress application on the BoeFly portal.

Watch this video for simple instructions on how to add an owner to a business application on the BoeFly PPP Portal.

There are some instances where we have decided to pivot loan applications from one BoeFly lender to another in an effort to expedite SBA approval. Status updates in the portal have oftentimes adjusted in connection with this. Do not be alarmed; status updates in the portal are often delayed due to feedback from our lending partners being delayed itself.

All of BoeFly’s lending partners remain fully focused on processing as many PPP applications as possible. Due to the nature of the SBA’s online authorization system (E-Tran), there has been a backlog of pushing approvals through. As such, the status updates in the BoeFly portal may be significantly delayed as they are dependent on BoeFly receiving details from our lending partners.

On April 30th, BoeFly sent an email to applicants that asks for their quick response to the question “Are you still in need of a PPP loan?” In order to expedite the process, make sure you respond.

All businesses – including nonprofits, veterans’ organizations, tribal business concerns, sole proprietorships, self-employed individuals, and independent contractors – with 500 or fewer employees can apply. Businesses in certain industries can have more than 500 employees if they meet applicable SBA employee-based size standards for those industries.

For this program, the SBA’s affiliation standards are waived for small businesses (1) in the hotel and food services industries; or (2) that are franchises in the SBA’s Franchise Directory; or (3) that receive financial assistance from small business investment companies licensed by the SBA. Additional guidance may be released as appropriate.

For additional SBA and Treasury guidance, the Treasury Department has created a link to their own FAQ document, to address specific borrower and lender questions concerning the implementation of the PPP, that will be updated on a regular basis.

You are eligible for a PPP loan if:

- you were in operation on February 15, 2020;

- you are an individual with self-employment income (such as an independent contractor or a sole proprietor);

- your principal place of residence is in the United States;

- and you filed or will file a Form 1040 Schedule C for 2019.

However, if you are a partner in a partnership, you may not submit a separate PPP loan application for yourself as a self-employed individual. Instead, the self-employment income of general active partners may be reported as a payroll cost, up to $100,000 annualized, on a PPP loan application filed by or on behalf of the partnership.

Partnerships are eligible for PPP loans under the Act, and the Administrator has determined, in consultation with the Secretary of the Treasury (Secretary), that limiting a partnership and its partners (and an LLC filing taxes as a partnership) to one PPP loan is necessary to help ensure that as many eligible borrowers as possible obtain PPP loans before the statutory deadline of June 30, 2020. This limitation will allow lenders to more quickly process applications and lessen the burdens of applying for partnerships/partners.

For additional guidance as an individual with self-employed income, please review the new interim final rule, issued on April 2, 2020, by the SBA, or visit their FAQs that are being updated periodically.

Your business must have been operational as of February 15, 2020, and had employees for whom you paid salaries and payroll taxes at that time or you are an individual with self-employment income (such as an independent contractor or a sole proprietor) and you filed or will file a Form 1040 Schedule C for 2019.

For businesses with employees:

Average monthly payroll costs, excluding compensation above $100,000 in wages (based on prior 12 months or from the calendar year 2019) X 2.5. That amount is subject to a $10 million cap.

In general, borrowers can calculate their aggregate payroll costs using data either from the previous 12 months or from calendar year 2019. For seasonal businesses, the applicant may use average monthly payroll for the period between February 15, 2019, or March 1, 2019, and June 30, 2019. An applicant that was not in business from February 15, 2019 to June 30, 2019 may use the average monthly payroll costs for the period January 1, 2020 through February 29, 2020.

Borrowers may use their average employment over the same time periods to determine their number of employees, for the purposes of applying an employee-based size standard. Alternatively, borrowers may elect to use SBA’s usual calculation: the average number of employees per pay period in the 12 completed calendar months prior to the date of the loan application (or the average number of employees for each of the pay periods that the business has been operational, if it has not been operational for 12 months).

Rent does not count as “payroll costs” and should not be included in your loan calculations. However, proceeds from the loan can be used for working capital.

For individuals with self-employment income (such as an independent contractor or a sole proprietor) who file a Form 1040, Schedule C:

How you calculate your maximum loan amount depends upon whether or not you employ other individuals. If you have no employees, the following methodology should be used to calculate your maximum loan amount:

- Find your 2019 IRS Form 1040 Schedule C line 31 net profit amount (if you have not yet filed a 2019 return, fill it out and compute the value). If this amount is over $100,000, reduce it to $100,000. If this amount is zero or less, you are not eligible for a PPP loan.

- Calculate the average monthly net profit amount (divide the amount from Step 1 by 12).

- Multiply the average monthly net profit amount from Step 2 by 2.5.

- Add the outstanding amount of any Economic Injury Disaster Loan (EIDL) made between January 31, 2020 and April 3, 2020 that you seek to refinance, less the amount of any advance under an EIDL COVID-19 loan (because it does not have to be repaid). Regardless of whether you have filed a 2019 tax return with the IRS, you must provide the 2019 Form 1040 Schedule C with your PPP loan application to substantiate the applied-for PPP loan amount and a 2019 IRS Form 1099-MISC detailing nonemployee compensation received (box 7), invoice, bank statement, or book of record that 7 establishes you are self-employed. You must provide a 2020 invoice, bank statement, or book of record to establish you were in operation on or around February 15, 2020.

If you have employees, the following methodology should be used to calculate your maximum loan amount:

- Compute 2019 payroll by adding the following:

- Your 2019 Form 1040 Schedule C line 31 net profit amount (if you have not yet filed a 2019 return, fill it out and compute the value), up to $100,000 annualized, if this amount is over $100,000, reduce it to $100,000, if this amount is less than zero, set this amount at zero;

- 2019 gross wages and tips paid to your employees whose principal place of residence is in the United States computed using 2019 IRS Form 941 Taxable Medicare wages & tips (line 5c- column 1) from each quarter plus any pre-tax employee contributions for health insurance or other fringe benefits excluded from Taxable Medicare wages & tips; subtract any amounts paid to any individual employee in excess of $100,000 annualized and any amounts paid to any employee whose principal place of residence is outside the United States; and

- 2019 employer health insurance contributions (health insurance component of Form 1040 Schedule C line 14), retirement contributions (Form 1040 Schedule C line 19), and state and local taxes assessed on employee compensation (primarily under state laws commonly referred to as the State Unemployment Tax Act or SUTA from state quarterly wage reporting forms).

- Calculate the average monthly amount (divide the amount from Step 1 by 12).

- Multiply the average monthly amount from Step 2 by 2.5.

- Add the outstanding amount of any EIDL made between January 31, 2020 and April 3, 2020 that you seek to refinance, less the amount of any advance under an EIDL COVID-19 loan (because it does not have to be repaid). You must supply your 2019 Form 1040 Schedule C, Form 941 (or other tax forms or equivalent payroll processor records containing similar information) and state quarterly wage unemployment insurance tax reporting forms from each quarter in 2019 or equivalent payroll processor records, along with evidence of any retirement and health insurance contributions, if applicable. A payroll statement or similar documentation from the pay period that covered February 15, 2020 must be provided to establish you were in operation on February 15, 2020.

- Salaries (up to $100,000* for any employee), wages, commissions or similar compensation, cash tips or equivalent, paid vacations, paid sick, parental and family medical leave

- Allowance for dismissal or separation

- Group health costs including insurance premiums

- Retirement benefits

- State and local payroll taxes

Any amounts that an eligible borrower has paid to an independent contractor or sole proprietor should be excluded from the eligible business’s payroll costs. However, an independent contractor or sole proprietor will itself be eligible for a loan under the PPP, if it satisfies the applicable requirements.

Rent does not count as “payroll costs” and should not be included in your loan calculations. However, proceeds from the loan can be used for working capital.

* The exclusion of compensation more than $100,000 annually applies only to cash compensation, not to non-cash benefits, including:

- employer contributions to defined-benefit or defined-contribution retirement plans;

- payment for the provision of employee benefits consisting of group health care coverage, including insurance premiums; and

- payment of state and local taxes assessed on compensation of employees.

No. Any amounts that an eligible borrower has paid to an independent contractor (1099 employee) or sole proprietor should be excluded from the eligible business’s payroll costs. However, an independent contractor or sole proprietor will itself be eligible for a loan under the PPP, if it satisfies the applicable requirements.

Under the Act, payroll costs are calculated on a gross basis without regard to (i.e., not including subtractions or additions based on) federal taxes imposed or withheld, such as the employee’s and employer’s share of Federal Insurance Contributions Act (FICA) and income taxes required to be withheld from employees.

As a result, payroll costs are not reduced by taxes imposed on an employee and required to be withheld by the employer, but payroll costs do not include the employer’s share of payroll tax. For example, an employee who earned $4,000 per month in gross wages, from which $500 in federal taxes was withheld, would count as $4,000 in payroll costs. The employee would receive $3,500, and $500 would be paid to the federal government. However, the employer-side federal payroll taxes imposed on the $4,000 in wages are excluded from payroll costs under the statute.

No personal guarantee; no collateral requirements.

1% fixed rate for a 2-year term. Principal and interest payments on the loan will be deferred for 6 months up to 12-months.

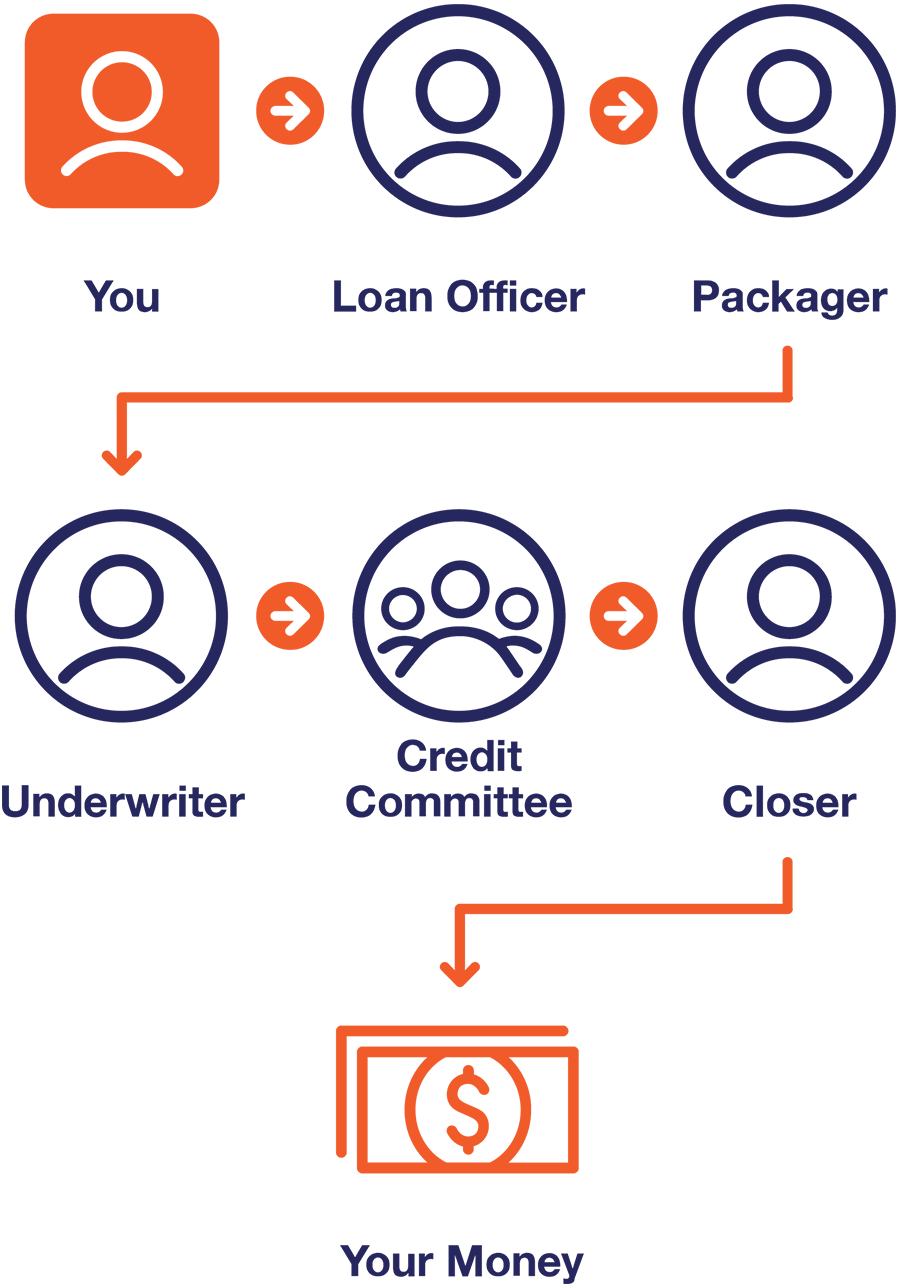

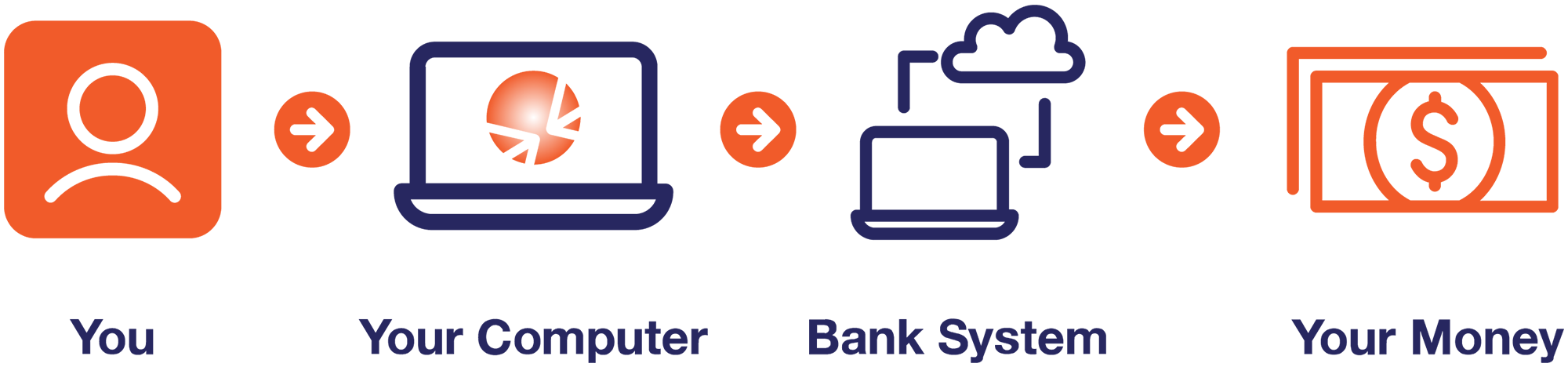

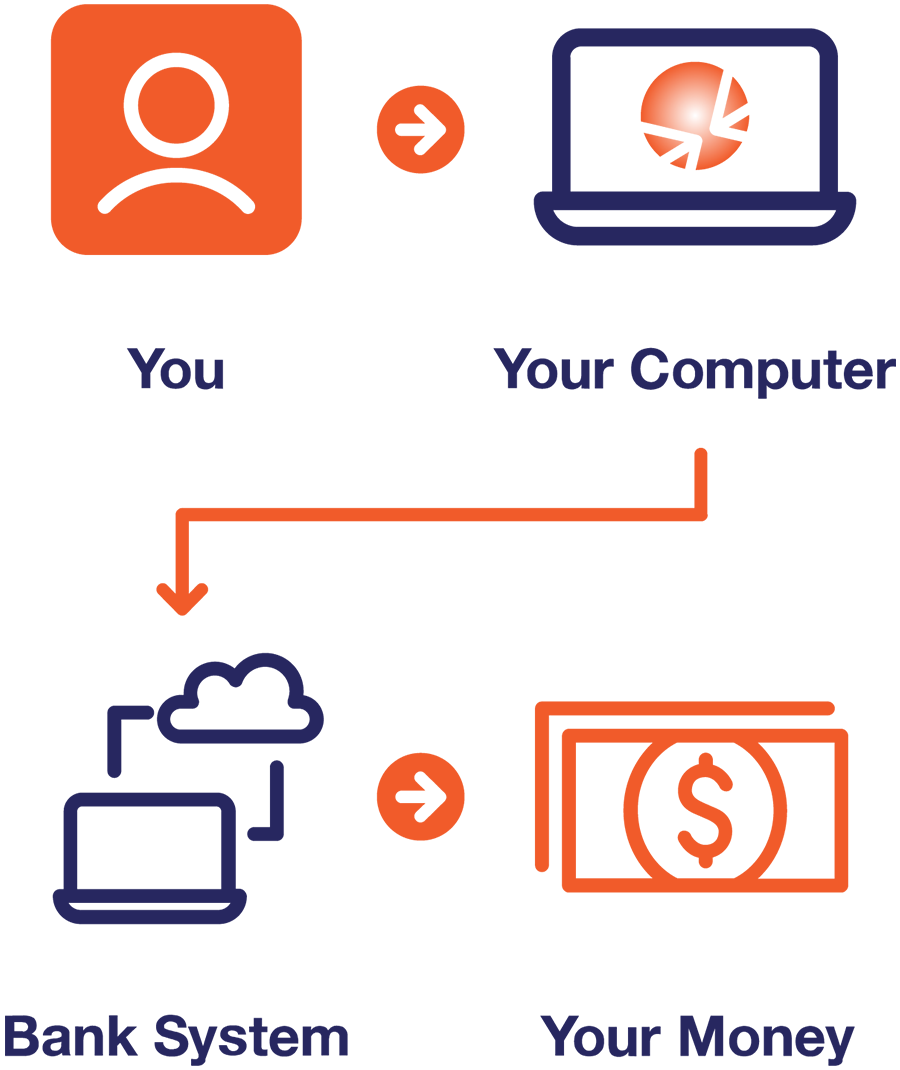

The majority of lenders can’t handle the high volume of loan applications, and this could delay getting you your money. Banks are unsettled and the pressure is intense on all parties, not to mention that banks are in crisis mode with COVID-19, just like you. BoeFly is continuing to work closely with both community banks and large national banks as they come online to process PPP loans. We process with an array of lenders of all sizes, working with those that can work with technology and are OK with the economics, showing that they are not avoiding the program.

How banks execute will be critical.

Will banks use their 'normal process' relying on people and manual steps?

Will banks use the tech-driven process and focus on speed?

If you expect you will get a loan from a bank because you meet their criteria, you can still move forward with their process, and we’ll also keep processing for you unless you get your authorization elsewhere.

If you expect you will get a loan from a bank because you meet their criteria, you can still move forward with their process, and we’ll also keep processing for you unless you get your authorization elsewhere.

No, an application is not an SBA authorization. SBA authorization will occur when you are assigned an Electronic Loan Processing (E-Tran) number. This means your funds are reserved, but technically, an E-Tran is an SBA loan guaranty origination/servicing solution that:

- Leverages internet technology to reduce the turnaround time on loan guaranty requests.

- Is integrated into your SBA software products and enables you to submit electronically from your existing screens.

- Provides increased efficiency and decreased costs in the loan guaranty origination and servicing processes.

The time from authorization to funding may vary widely.

No, you do not need to complete that form. Instead, the documentation that you provide to BoeFly in your secure portal will be completing the necessary information found on that form.

At BoeFly, we pride ourselves on quick response times and providing excellent customer service. However, with the extremely high volume of PPP loan applicants, we cannot at this time respond to all direct inquiries while still being able to process as many loan applications as possible - which is currently our number one priority. Once you complete your application, you will receive ongoing communications from BoeFly with timely updates from the SBA and lenders. We urge you to utilize this robust FAQ page to try and locate the answer to your inquiry.

No. Providing an accurate calculation of payroll costs is the responsibility of the borrower, and the borrower must attest to the accuracy of those calculations. Lenders are expected to perform a good faith review, in a reasonable time frame, of the borrower’s calculations and supporting documents concerning average monthly payroll cost. The level of diligence by a lender should be informed by the quality of supporting documents supplied by the borrower. Minimal review of calculations based on a payroll report by a recognized third-party payroll processor, for example, would be reasonable.

If lenders identify errors in the borrower’s calculation or material lack of substantiation in the borrower’s supporting documents, the lender should work with the borrower to remedy the error.

No. It is the responsibility of the borrower to determine which entities (if any) are its affiliates and determine the employee headcount of the borrower and its affiliates. Lenders are permitted to rely on borrowers’ certifications.

Yes. Borrowers must apply the affiliation rules set forth in SBA’s Interim Final Rule on Affiliation. A borrower must certify on the Borrower Application Form that the borrower is eligible to receive a PPP loan, and that certification means that the borrower is a small business concern as defined in section 3 of the Small Business Act, meets the applicable SBA employee-based or revenue-based size standard, or meets the tests in SBA’s alternative size standard, after applying the affiliation rules, if applicable.